Tuesday, December 10, 2013

Tuesday, September 17, 2013

8 tips for Using Feng Shui

The ancient Chinese art of feng shui (pronounced “fung shway”) is over 3,000 years old, and has been known to help many REALTORS® sell homes when applied to their listings. This method of arranging inner and outer environments so they consistently support the possibility of all the good things in life encourages health, wealth, great relationships, career, and wisdom – just to name a few. Karen Rauch Carter, author of the bestselling book Move Your Stuff, Change Your Life, works with many REALTORS® who swear by her techniques. Here are a few easy fixes to help prepare your listings for sale the feng shui way.

1. Create a happy front door. According to feng shui principles, the easier it is for people to bring opportunities to your front door, the more you’ll have. Make the walk from the car to the front door a delightful experience. That means no thorny plants nearby, no sidewalk trippers, and no cobwebs to walk through. Next, add details that draw people to the front door, such as a welcome mat and flowers. You might even consider painting the front door a shade of red to attract positive energy, especially if it’s positioned in shadow or under an overhang or porch. Make sure the doorbell and outdoor lights are in good, working order. Clean the door and stoop thoroughly -- shine the metal on the knocker, wash any windows -- make it the prettiest front door on the block!

2. Fix the leaks. This is, of course, basic common sense, but in feng shui leaking water is equivalent to leaking money. When a leak is fixed, the money stays, and you may just end up selling the home at a higher price.

3. For every room, a true function. When buyers see a treadmill in the bedroom, a computer on the kitchen counter, or a bike in the hallway, it may appear that the house doesn’t seem to have enough room for all the necessary functions. When staging a home, make sure every object in the room matches the room’s function.

4. Manage outdoor plants. Plants, especially dead ones, can block positive energy when physically touching the outside of the house. When the limbs of a tree are in direct contact, they may even transfer negative energy into the home. Remove worry and excess debris, and the house may sell faster.

5. Place furniture in a commanding position. This means different things for different rooms, but the feng shui basic premise is that furniture should be arranged so the back and head are protected. Don’t have your back to a door or window when you’re on a couch, chair, or bed, and avoid directly facing a wall, especially when sitting at your desk.

6. Keep the energy flowing. Doors and windows are the entry points for energy to enter or escape, so make sure all are in good working order to encourage positive energy flow. All doors (including closets) should open freely with nothing blocking their way. Windows should be easy to open – make sure none are painted or nailed shut. If they’re stuck, you might get stuck with a listing that’s hard to sell. If possible, open curtains and blinds before a showing to invite energy into the home.

7. Let the buyer find the view. When a home is designed to give you that big WOW view upon entering the front door, consider creating a bold, dramatic design statement to compete for that attention somewhere inside the home. This may seem counter-intuitive, but if buyers are immediately drawn outside, that means nothing inside is holding their attention. The more you can keep attention INSIDE the house before the eyes slip outside, the better energy and "greater likeability" you are creating.

8. Employ the power of red. Homes lacking a fire element may be more difficult to sell. This problem can be addressed with a quick fix of adding red or hot orange colors where appropriate. Place a vase of red flowers on the counter, or toss a few red throw pillows on the couch or bed if the décor allows. A bowl of red apples is another easy solution. Pointy, triangular shapes are also considered fire elements in feng shui, so consider filling a vase with flowers like birds of paradise. Animal prints can also provide a fire element, as can actual fire, such as candles. Try adding a few splashes of red here and there, and see what it can do for your next listing.

Saturday, September 7, 2013

How to Buy and Sell a Home at the Same Time

Like Lili Chen on facebook

Now that the real estate market is picking up again, many people are looking to sell their homes at last. But when you sell, you have to move somewhere — which usually means buying another home. Buying and selling at the same time brings up a whole new set of challenges, but those who plan well in advance can make it happen smoothly.

Here are five ways to successfully buy and sell a home at the same time.

1. Prepare to be stressed

Buying a home is stressful. Selling a home is stressful. When you do both at the same time, the experience is super stressful, not to mention emotional and difficult on many levels. You’re potentially carrying two mortgages or trying to time the purchase with the sale. There will be a lot of sleepless nights, worrying over finances and pressure to make a decision. It’s enough to ignite a family war.Accepting upfront that this process will be extremely stressful will help in the long run. Know that most homeowners go through this, and there is success at the end of the long, dark tunnel. Plan everything as much as possible in advance. Do your homework. And take care of yourself. You’re going to be busier than usual.

2. Meet with your agent early on

Owners often believe their home is worth less than what the current market will bear. That’s why it’s important to meet with your real estate agent early on, even months before you plan to buy or sell. Researching online valuation tools or doing basic research will help to guide you. But a local agent will help you understand your home’s true current market value and marketability. A good agent is in the trenches daily and knows your neighborhood and market inside and out.3. Learn the market where you want to purchase

After getting some hard numbers for your home’s sale you need to do the same on the purchase side. What’s on your wish list? What are your priorities? Determine your needs and understand what you will get for your money on the purchase side. You need to know this to factor in how financing will work with the buy/sell. Also, understand that market. Is it more or less competitive than where you live now? How long can you expect to search for a home? This will factor into your sale timing. If you’re moving within the city or town where you live, your listing agent will likely serve as your buying agent. If you’re moving just outside your area, you may need to ask your agent to refer you to an agent knowledgeable about that area.4. Know your numbers

Once you understand the numbers on both the purchase and the sale, you need to know your financing options. Many people today don’t have a strong-enough financial foundation to purchase another home before selling their own, so knowing this upfront can help you plan more appropriately.Engage a local mortgage broker or lender and understand what kind of down payment you’ll need to make a purchase, given the price point and type of home you seek to buy. How much equity do you have in your current home, and is the equity available? Do you have enough of a down payment liquid and would a lender allow you to make the purchase before selling the home? Find out by going through the loan pre-approval process. A good, local mortgage professional is as valuable as a good real estate agent.

5. Make a plan

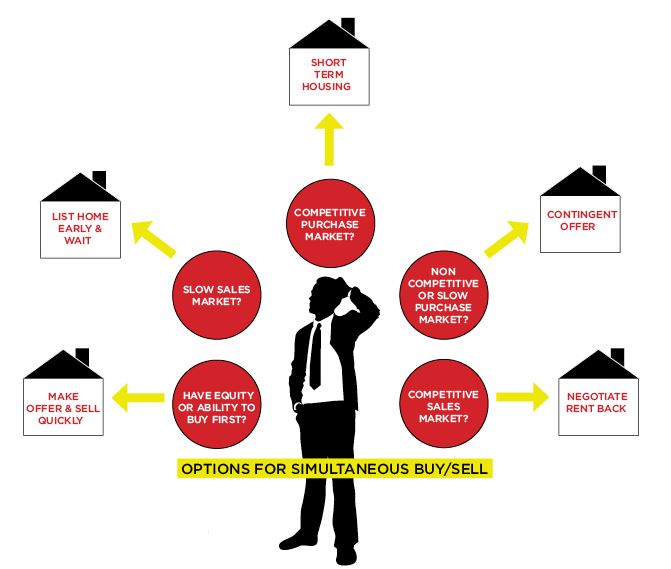

Now that you know your numbers, it’s time to come up with a plan and execute. The plan can vary greatly, depending upon any number of conditions. Some examples:- Buying in a competitive market? Adding a contingency that your current home must sell before you buy probably won’t work.

- Selling in a competitive market? You may be able to negotiate with the buyer for a longer escrow or even a rent back. This would buy you time on the purchase side.

- Selling in a slow market and buying in a competitive market? Need the sales proceeds in order to do the purchase? Unfortunately, you’re in the worst-case scenario. Consider the option of selling your home first and moving into temporary housing. While not the most physically convenient, it could be less stressful.

- Need temporary housing? Start researching those options now well in advance

Understanding the variables

There are so many variables that can come into play when buying or selling. Each one may affect your decision-making process. Identifying and planning for the variables as much as possible early on will help you avoid sleepless nights, stressful days, or fights with your spouse or partner.Author: Brendon DeSimone

Friday, September 6, 2013

Top 5 Mistakes Home Buyers Make — And How to Avoid Them

From the beginning of your home search through closing escrow, there’s an awful lot to think about and do. It’s not unusual to make a mistake along the way. But with the financial stakes so high, a false move can end up costing you a lot of money.

Here are five common home buyer mistakes, with tips on how to avoid them.

This strategy may work sometimes, especially in a weak seller’s market. But we’re in a competitive market for buyers now, so don’t count on it. The seller most likely will have a backup offer from another buyer who really wants the home — and who is hoping your deal falls through. If you start asking for unwarranted credits, the seller may simply go with the backup offer, leaving you out in the cold.

A better strategy: Make your best offer, and don’t assume you can negotiate it down later.

The buyer ended up walking away from the deal. The house sold soon after at a higher price than what was negotiated with the first buyer.

Of course, you should ask for credits if an inspection turns up potentially costly repair work you didn’t know about when you made your offer. But even in a buyer’s market, don’t assume you can get sellers to cave in to unreasonable demands at the last minute.

For example, a renter in San Francisco spent three years looking for the best “deal” she could possibly get, passing up many good opportunities. Eventually, her landlord wanted to sell the place she was renting. This forced her to finally buy, but under pressure. She ended up buying at the top of the market. If she hadn’t held out for so long in hopes of scoring an amazing deal, she’d have saved herself a lot of money and time. She’d even have built up some equity in a home over those three years.

In a strong real estate market, the deals are in homes that have been overpriced and haven’t sold as a result, and/or properties that don’t show well because they need work. If the home you want is well-priced, in a good neighborhood and doesn’t need much work, the best strategy is to make a solid offer and be prepared to go over asking if necessary.

But this strategy often backfires. First of all, the real estate agent’s role isn’t just about finding listings. With Internet access, buyers can easily find listings themselves. The agent’s role today is more about presenting your offer to the seller’s agent in a way that will help get it accepted and making sure it sticks through an escrow.

A savvy agent knows the ins and outs of the local market better than an uninformed buyer with a full-time job and family. A good agent will know the back-stories behind the comps, for example. He or she will know that a comparable home sold for 5 percent less (than the home you’re considering) only because the sellers were divorcing, or the property had a retaining wall problem. Without an agent, you’d simply see that the comparable home sold for 5 percent less. You might ask the seller of the home to match that 5 percent reduction — and you’d be surprised when the seller says, “No thanks.”

Also, experienced agents have a strong network in the local market, which can give you an added edge. Good agents like to work with other good agents. And if nothing else, keep in mind that a listing agent might not even consider working with an unrepresented buyer.

Finally, the seller pays the buyer’s real estate commission, so having an agent for your home search costs you nothing anyway. Most importantly, there’s bound to come a time during the complicated real estate transaction when you have serious doubts or big questions. Your agent can be the trusted adviser you need to walk you through the maze.

Case in point: In 2005, a buyer in San Francisco bought a home with no garage. The house was on multiple transit lines, he used his bicycle to get around and he knew he’d have access to a leased garage space if he needed it. So he felt he didn’t need a garage.

Three years later, the market was slower, but the owner had to sell. He didn’t feel his home should be priced less than a comparable property with a deeded garage because his house was so centrally located. Plus, he had that leased garage space to offer. The problem was, many buyers drive to work, and they don’t want to risk losing a leased garage space. The result was that many buyers wouldn’t even look at his home’s photos online, let alone go to the open house — because it lacked a garage.

So when you’re buying a home, put yourself in a potential seller’s shoes. The last thing you want is to buy a dream home that becomes a nightmare when it’s time to sell.

This article write by :Brendon DeSimone ; Share by: Lili Chen.

Here are five common home buyer mistakes, with tips on how to avoid them.

You expect to get the price down after making an offer

The real estate market is heating up across the country. In many markets, homes are selling for more than asking price. Some buyers win the bidding war by going over asking — only to try to negotiate the price down by asking for credits during escrow.This strategy may work sometimes, especially in a weak seller’s market. But we’re in a competitive market for buyers now, so don’t count on it. The seller most likely will have a backup offer from another buyer who really wants the home — and who is hoping your deal falls through. If you start asking for unwarranted credits, the seller may simply go with the backup offer, leaving you out in the cold.

A better strategy: Make your best offer, and don’t assume you can negotiate it down later.

You wait until the eleventh hour to ask for credits

In Houston, a seller had put his house on the market with full disclosure that it had termites. A buyer made an offer and went into contract with the seller. After further inspections, and at the eleventh hour, the buyer demanded an unreasonable amount be deducted from the sale price. The buyer assumed that the seller, not wanting to put the house on the market again, would agree, just to close the deal. But that’s not what happened. The seller agreed to reduce the price, but not by the full amount the buyer wanted.The buyer ended up walking away from the deal. The house sold soon after at a higher price than what was negotiated with the first buyer.

Of course, you should ask for credits if an inspection turns up potentially costly repair work you didn’t know about when you made your offer. But even in a buyer’s market, don’t assume you can get sellers to cave in to unreasonable demands at the last minute.

You chase a deal at all costs

Everyone wants to save money, especially on a high-ticket item such as real estate. Unfortunately, this causes some would-be buyers to make lowball offers in hopes of getting a “deal.” Or, potential buyers lose out on homes they might have been able to get otherwise, which ends up costing money in the long run.For example, a renter in San Francisco spent three years looking for the best “deal” she could possibly get, passing up many good opportunities. Eventually, her landlord wanted to sell the place she was renting. This forced her to finally buy, but under pressure. She ended up buying at the top of the market. If she hadn’t held out for so long in hopes of scoring an amazing deal, she’d have saved herself a lot of money and time. She’d even have built up some equity in a home over those three years.

In a strong real estate market, the deals are in homes that have been overpriced and haven’t sold as a result, and/or properties that don’t show well because they need work. If the home you want is well-priced, in a good neighborhood and doesn’t need much work, the best strategy is to make a solid offer and be prepared to go over asking if necessary.

You think you can do it all yourself

With so much information about homes available online today, many people, such as tech-savvy Gen X and Gen Y home buyers, may assume they can buy a home without a real estate agent’s help.But this strategy often backfires. First of all, the real estate agent’s role isn’t just about finding listings. With Internet access, buyers can easily find listings themselves. The agent’s role today is more about presenting your offer to the seller’s agent in a way that will help get it accepted and making sure it sticks through an escrow.

A savvy agent knows the ins and outs of the local market better than an uninformed buyer with a full-time job and family. A good agent will know the back-stories behind the comps, for example. He or she will know that a comparable home sold for 5 percent less (than the home you’re considering) only because the sellers were divorcing, or the property had a retaining wall problem. Without an agent, you’d simply see that the comparable home sold for 5 percent less. You might ask the seller of the home to match that 5 percent reduction — and you’d be surprised when the seller says, “No thanks.”

Also, experienced agents have a strong network in the local market, which can give you an added edge. Good agents like to work with other good agents. And if nothing else, keep in mind that a listing agent might not even consider working with an unrepresented buyer.

Finally, the seller pays the buyer’s real estate commission, so having an agent for your home search costs you nothing anyway. Most importantly, there’s bound to come a time during the complicated real estate transaction when you have serious doubts or big questions. Your agent can be the trusted adviser you need to walk you through the maze.

You don’t think like a seller

Most likely, at some point in the future you’ll need to sell the home you’re about to buy. That’s why it’s important to think like a potential seller as well as a buyer.Case in point: In 2005, a buyer in San Francisco bought a home with no garage. The house was on multiple transit lines, he used his bicycle to get around and he knew he’d have access to a leased garage space if he needed it. So he felt he didn’t need a garage.

Three years later, the market was slower, but the owner had to sell. He didn’t feel his home should be priced less than a comparable property with a deeded garage because his house was so centrally located. Plus, he had that leased garage space to offer. The problem was, many buyers drive to work, and they don’t want to risk losing a leased garage space. The result was that many buyers wouldn’t even look at his home’s photos online, let alone go to the open house — because it lacked a garage.

So when you’re buying a home, put yourself in a potential seller’s shoes. The last thing you want is to buy a dream home that becomes a nightmare when it’s time to sell.

This article write by :Brendon DeSimone ; Share by: Lili Chen.

Tuesday, July 16, 2013

3 Things That Make the Best Real Estate Investment

A couple of weeks ago I wrote The 6 Worst Types of Real Estate Investments

that covered the types of properties an investor should avoid. Today I

will cover what makes up a really good real estate investment.

In

general you probably want to earn wealth on real estate based on risk

you are taking, while minimizing the amount of time you need to spend

attending to the property. In order to accomplish this, you need to make

some smart choices upfront when buying investment property. Your goal

should be to strive to get as close as possible on as many of these

optimal scenarios as possible:

In

general you probably want to earn wealth on real estate based on risk

you are taking, while minimizing the amount of time you need to spend

attending to the property. In order to accomplish this, you need to make

some smart choices upfront when buying investment property. Your goal

should be to strive to get as close as possible on as many of these

optimal scenarios as possible:

Pays a Fair Cash-on-Cash Return

When you buy property you are taking money out of your liquid

financial assets – stocks, bonds, CDs – and investing it into a very

illiquid asset – real estate. You were earning a rate of return on your

financial assets, such as 4 percent or 6 percent, and you should strive

to earn a fair cash-on-cash rate of return on your real estate. To do

this, you need to pro forma your deals and buy cash flow-positive

properties that earn you decent returns – not those prize properties

that are negative, negative, negative. For more guidance on this, see Smart Investing – A Tale of Two Townhomes.

It’s the nice, boring, wholly owned, in good shape, cash flow-positive properties that are the best investments. They are out there for your picking, but it’s not as simple as finding a property on the MLS and buying it.

You need to do some hard work, research, read up, and make smart, educated decisions to acquire the best real estate investments!

In

general you probably want to earn wealth on real estate based on risk

you are taking, while minimizing the amount of time you need to spend

attending to the property. In order to accomplish this, you need to make

some smart choices upfront when buying investment property. Your goal

should be to strive to get as close as possible on as many of these

optimal scenarios as possible:

In

general you probably want to earn wealth on real estate based on risk

you are taking, while minimizing the amount of time you need to spend

attending to the property. In order to accomplish this, you need to make

some smart choices upfront when buying investment property. Your goal

should be to strive to get as close as possible on as many of these

optimal scenarios as possible:

Pays a Fair Cash-on-Cash Return

When you buy property you are taking money out of your liquid

financial assets – stocks, bonds, CDs – and investing it into a very

illiquid asset – real estate. You were earning a rate of return on your

financial assets, such as 4 percent or 6 percent, and you should strive

to earn a fair cash-on-cash rate of return on your real estate. To do

this, you need to pro forma your deals and buy cash flow-positive

properties that earn you decent returns – not those prize properties

that are negative, negative, negative. For more guidance on this, see Smart Investing – A Tale of Two Townhomes.Isn’t Too Risky an Investment

All real estate is extremely high risk. Development of real estate, land, Tenant-In-Common (TIC) investments, private real estate funds, fixer uppers, etc., all have much higher risk profiles than just simply buying a nice established cash flow investment property. In many of those investments, you will never see a dime of your money again because there are just so many things that can go wrong! So if you want to own real estate, consider simply taking fee simple title in your own name – or an entity you wholly own – to the properties you purchase. In addition, you must do the proper due diligence, analyze, test, review reports, etc., to make a lower risk real estate decision.Doesn’t Require a Lot of Time or Managing

Some properties just require way too much time and management to make them smart investments. Examples include vacation rentals, low quality properties in bad areas, college rentals, etc. Nice boring properties rented for as long as possible to decent credit profile tenants seem to take the least time to manage. In addition, treating your tenants fairly and with respect goes a long way towards keeping good relations with them; and reducing your hassles when there is an issue you need to address. And believe me — there will be issues!It’s the nice, boring, wholly owned, in good shape, cash flow-positive properties that are the best investments. They are out there for your picking, but it’s not as simple as finding a property on the MLS and buying it.

You need to do some hard work, research, read up, and make smart, educated decisions to acquire the best real estate investments!

Sunday, July 14, 2013

Real Estate Investing: Why Cash Flow Is King

As real estate values rise nationwide and many properties listed for

sale are being fought over by investors and home buyers, it seems that,

once again, investment property buyers are paying outrageous prices for

properties. Anyone recall this phenomenon in 2004, 2005 and 2006?

An “outrageous price” is one that is way too high considering the cash flows the rental property can generate. These negative cash flow properties are rarely profitable investments, compared with other investment options a buyer could have chosen.

Experienced real estate investors only buy properties that are cash-flow positive — based on conservative estimates — and skip those pesky negative cash flow deals. Note that those negative cash flow properties are typically the fancy prize properties in town; you know, the location, location, location properties.

As an example, let’s say an investor buys a $125,000 house by investing cash equity of $40,000 (25 percent down payment plus closing costs and rehabilitation costs) that generates rental income of $1,200 per month. The mortgage plus other operating expenses total $1,015 per month. So the rent less all the expenses leaves $185 of positive monthly income, or $2,220 per year. If we divide this $2,220 annual cash flow by the $40,000 initial cash investment, it calculates to a cash-on-cash return of 5.55 percent — a pretty fair deal on a decent real estate investment.

And with that nice positive cash flow, you also will get some extra return yield as a result of the amortization of your mortgage. Plus you probably will get some tax benefits and possibly some appreciation in value too.

Cash flow is king, and if you buy positive cash flow properties, you will feel like royalty each month as your bank account balance builds up and you earn wealth over the years!

An “outrageous price” is one that is way too high considering the cash flows the rental property can generate. These negative cash flow properties are rarely profitable investments, compared with other investment options a buyer could have chosen.

Experienced real estate investors only buy properties that are cash-flow positive — based on conservative estimates — and skip those pesky negative cash flow deals. Note that those negative cash flow properties are typically the fancy prize properties in town; you know, the location, location, location properties.

Penciling out a deal

The main reason investors keep paying these high prices is because 95 percent of them acquire properties without doing any financial analysis to determine whether the property will actually produce decent investment returns. Instead, they hope that a property will go up in value, they’ll sell it and make a bundle. Unfortunately, that scenario rarely happens.As an example, let’s say an investor buys a $125,000 house by investing cash equity of $40,000 (25 percent down payment plus closing costs and rehabilitation costs) that generates rental income of $1,200 per month. The mortgage plus other operating expenses total $1,015 per month. So the rent less all the expenses leaves $185 of positive monthly income, or $2,220 per year. If we divide this $2,220 annual cash flow by the $40,000 initial cash investment, it calculates to a cash-on-cash return of 5.55 percent — a pretty fair deal on a decent real estate investment.

Additional perks

Only about half of the properties in a general marketplace would generate positive cash flows and a decent, actual return such as 5.55 percent. In actuality, real estate investing is much more complicated than just penciling out your cash-on-cash return, but that analysis is a good start.And with that nice positive cash flow, you also will get some extra return yield as a result of the amortization of your mortgage. Plus you probably will get some tax benefits and possibly some appreciation in value too.

Cash flow is king, and if you buy positive cash flow properties, you will feel like royalty each month as your bank account balance builds up and you earn wealth over the years!

Saturday, July 13, 2013

How to Make a Better Real Estate Investment

Investing in real estate has lots of risks that can derail even the

best-looking deals, so you need to make sure you are addressing the

known perils and doing the hard work to diminish the chances that

something will go astray with your purchase. And here’s the most

important part: You must start before making the purchase and continue during ownership.

So, if you want to make a better real estate investment, the areas above are good places to start. You’re reducing the likelihood of property issues occurring that could cause you financial pain or take up an inordinate amount of your time. And if you talk to long-term investors — and you should do that, too, to pick their brains — they’ll probably have many “I learned that lesson” stories to share. It’s better to learn these lessons from other investors than to learn them the hard way during your property ownership.

Financial sense

When you buy real estate, you must make sure that it’s a smart financial decision. Rentals make sense if they are cash-flow positive and provide a fair rate of return on the invested equity. Investors should not purchase negative cash flow properties, period. If you pencil out your rate of return on a negative cash flow property, you’d probably realize it would have been better to invest your money elsewhere in an asset with better returns.Buy a property in good shape

Skip the fixer-uppers: They almost always cost way too much to repair. Many a buyer has theorized that it would be fun and profitable to buy a property, fix it up and sell it at a profit. Rarely does this scenario come true — usually the buyer ends up losing money. This may work for a construction contractor who is experienced in estimating the costs of repair, but for the Average Joe, chances are you will lose your money.Secure long-term financing

Make sure to take out long-term fixed interest rate financing. It costs significant amounts of money every time you finance or refinance a property, so try to do just one financing at purchase and enjoy the peace of mind knowing you won’t have to worry about interest rate changes in the future. Go long!Review your title documents

All buyers should review the title insurance policy, schedule of exclusions, title abstract and a plat or survey of the property. Schedule an hour for your title insurance agent to go through all those items with you, in detail, so you can address any issues before you purchase. Significant issues are rare, but you have to address them before you close escrow.Property and liability insurance

Make sure to keep the proper insurance in place and for an appropriate amount, as needed for the specific property and your specific circumstances. You should sit down with your insurance agent and discuss your complete financial and insurance picture so that if something does happen — such as a fire, dog bite, flood or slip-and-fall — your insurance company will work with you to reduce the chances it would significantly impact your finances.Manage rentals well

If your property is a rental, make sure to secure good tenants and keep them for as long as possible. Treat them well, keep your property in good shape, address issues and resolve them quickly. You’ll make the most money with the least hassle by treating your tenants the way you’d like to be treated.So, if you want to make a better real estate investment, the areas above are good places to start. You’re reducing the likelihood of property issues occurring that could cause you financial pain or take up an inordinate amount of your time. And if you talk to long-term investors — and you should do that, too, to pick their brains — they’ll probably have many “I learned that lesson” stories to share. It’s better to learn these lessons from other investors than to learn them the hard way during your property ownership.

Subscribe to:

Posts (Atom)